When you’re one of several 202,000,000 Americans you to definitely individual a home step one , you’re certain accustomed this new caveats of your own Western Dream. One of the most popular is the well known home loan.

While the average U.S. home loan personal debt for each debtor in the 2019 is up to $202,000, for each county can make an alternative sum to that particular figure. Ca, eg, retains the typical mortgage equilibrium from $364,000 if you find yourself New york simply clocks into the at the $162,000 dos .

The entire mediocre real estate loan debt is rising but not, averaging $184,000 within the 2015 in order to $202,000 in the 2019 across the country. With additional and money on the newest range, it’s not hard to understand why anyone may want to diving on one possible opportunity to straight down its commission or availability equity. Prior to diving from inside the, there are important matters to take on in advance of refinancing the financial.

Bankrate talks of an effective re-finance since the method in which you to loan is replaced because of the yet another financing, usually with positive terminology. 3 Therefore, home financing refinance is the approach regarding replacing a quicker favorable mortgage that have something finest fitted to your situation. Will this happens as a result of all the way down interest rates, however, there is most other explanations also.

There are many reasons you may re-finance your home loan. Decreasing the rate of interest, removing PMI, reducing monthly payments, combining debt, and opening collateral are some of the typical explanations.

These types of grounds had been detailed for the site and you may shouldn’t be taken because the an advice. Because you could potentially re-finance your house in order to consolidate personal debt, for example, doesn’t mean that you should. Work with these scenarios by the monetary coordinator to see whether a good refinance is during the best notice.

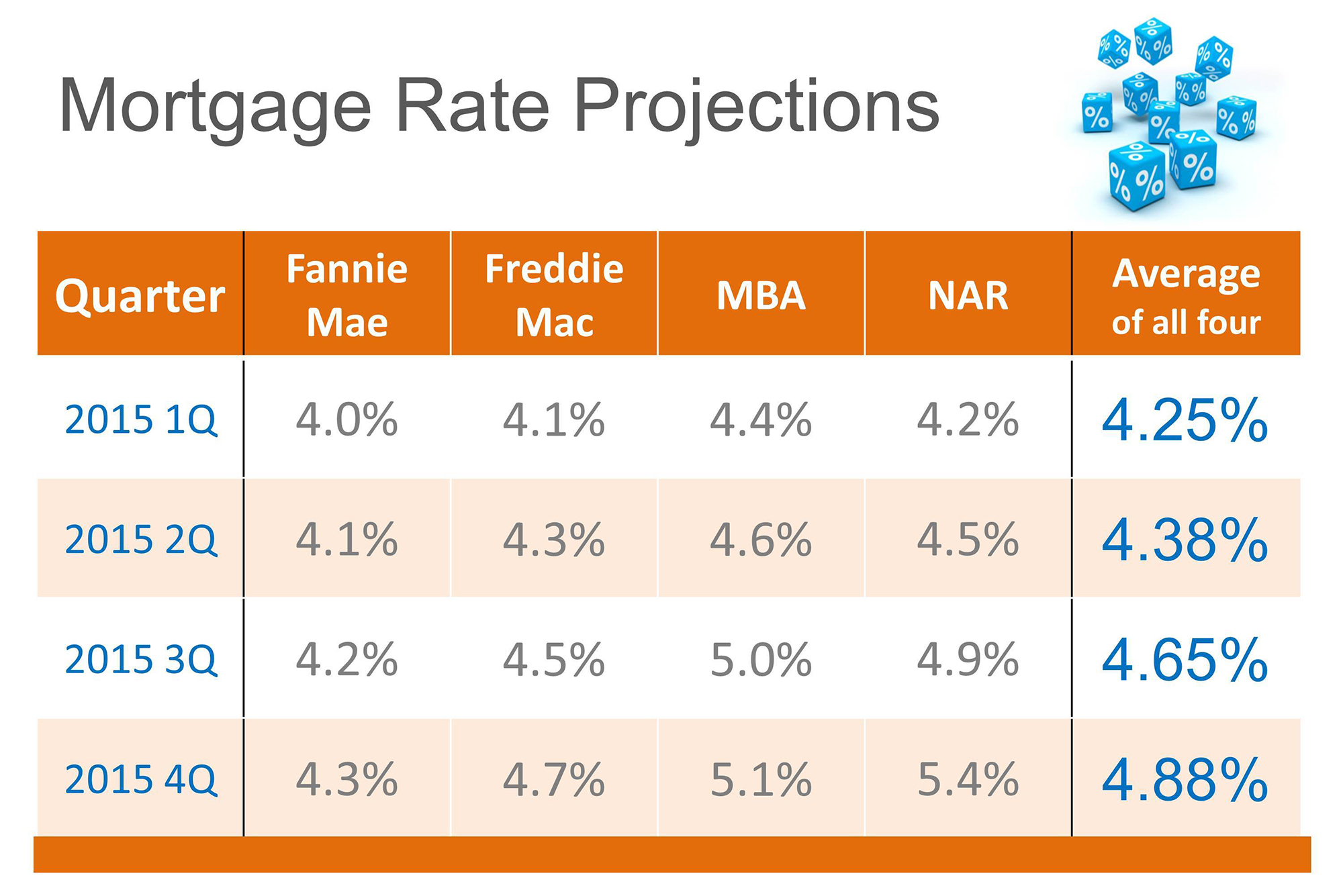

The common mortgage rate of interest during the 2008 is 6.03%, dropping to help you 4.54% 10 years afterwards into the 2018 cuatro . Although this atic changes, it is. The brand new visual below suggests the latest projected economic feeling made for the a good home loan balance off $200k, $350k, and you may $500k into the seasons step one:

These types of deals will be high stretched-out more than payday loan Remlap a 30-year period. Because difference with the a lot of time-identity websites well worth is evident, instantaneous gratification try acquired in the straight down payment per month. Including, a good $350,000 30-season financial get a principal and notice payment per month out-of $2,105 within 6.03%, while a speeds away from cuatro.54% will need a payment of $step 1,782. It month-to-month huge difference regarding $323 can have a content effect on your quality of life.

With respect to the User Financial Safety Agency, PMI often is called for if you have a normal loan and you can generate a downpayment off lower than 20 percent of your own house’s price. If you find yourself refinancing having a normal financing plus guarantee are less than 20% of worth of your home, PMI is also usually called for.

Particular lenders give a supply that enables one to see aside of your own PMI demands; which is, if your family worthy of values outside the 20% equity tolerance you happen to be capable consult so it be eliminated.

Although this work for pertains to certain, it doesn’t apply to all the. Alternatively, lenders will want good refinance to be sure the purchase price (otherwise re-finance worth) is reflective of the high valuation.

While the already talked about, decreasing the rate of interest relevant on financing is a superb answer to slow down the monthly obligations. There are two even more an effective way to decrease your payment.

"Sky Tour" company has successfully been working in the tourist market of Tajikistan since February 2011. Despite a relatively short period of activity, the company has thousands of organized trips and satisfied customers. We provide a wide range of tourist services, from excursions around Tajikistan, to round-the-world travel. We organize travel for every taste and depending on the wishes, we select the most ideal variant for the tourist. Managers of the company "Sky Tour" are highly qualified professionals, experts in their work and work execution is impeccable. We track every stage of the journey of our tourists and in the event of unforeseen situations we quickly resolve the issues that have arisen. "Sky Tour" company successfully cooperates with tour companies in all regions of Tajikistan, and many Tour Operators in all corners of the world which gives an opportunity to expand the range of services and choice of countries for recreation. Our goal is to make your trip highly comfortable, safe, and interesting. "Sky Tour" company is a member of the TATO (Tajik Association of Tour Operators) and is accredited with the Ministry of Foreign Affairs of the Republic of Tajikistan.

English

English Русский

Русский العربية

العربية